Merchant Services, Point of Sale...how does it all work?

Here’s the expanded, full version for your post:

What Are Merchant Services?

Many business owners swipe cards every day without realizing how many layers sit between that tap and the money landing in the bank. Three players make the system work: the point-of-sale system (POS), the merchant services provider, and the bank. Each one takes a fee, controls part of the process, and can either help or hurt your cash flow.

1. Point-of-Sale Systems

The POS is the front-end — hardware and software where transactions happen. Square, Clover, Toast, Lightspeed, and others all do roughly the same thing: collect the payment data, total the sale, and push that data to your merchant processor.

Modern POS systems often bundle merchant services, locking you into their processor. They’ll say it’s “included,” but it isn’t free. You’re paying through their processing rate.

If your volume is high enough, you can shop your POS separately from your merchant processor. That gives you control of both technology and pricing. The key question to ask: “Can I bring my own merchant account?” If the answer is no, you’re locked into their rates.

2. Merchant Services Providers

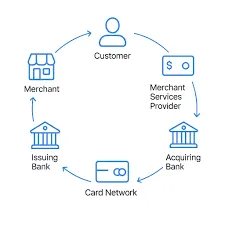

This is the middle layer that actually moves the money.

When you run a card, the merchant provider:

Sends the authorization to the card network (Visa, Mastercard, AmEx, Discover).

Receives confirmation the cardholder’s bank will pay.

Collects the funds in its settlement account.

Sends you the total minus fees, usually within one or two business days.

Typical Fee Structure

Merchant pricing has three parts:

Interchange: set by the card brands, roughly 1.5%–3%, depending on card type and risk. Non-negotiable.

Assessment Fees: network costs around 0.13%–0.15%. Also fixed.

Processor Markup: your negotiable piece. Usually 0.10%–0.50% + 5–10¢ per transaction on top of interchange.

So if you see “flat 2.9% + 30¢” pricing (Square, Stripe), that’s just a simplified blend of those three components with a healthy markup.

How to Save

Interchange-Plus Pricing: Ask for it. You’ll see each card’s true cost plus a disclosed markup. It’s transparent and almost always cheaper than bundled rates.

Batch Daily: Avoid per-transaction batching fees and reduce hold times.

Avoid High-Risk Categories: Rewards and business cards carry higher interchange. Debit is cheaper.

Negotiate Monthly Fees: Statement fees, PCI compliance, and junk add-ons add up fast.

Review Effective Rate: Divide total fees by total volume. If it’s over 3%, you’re likely overpaying.

3. The Bank

Your business bank isn’t processing cards; it’s the endpoint. The merchant provider sends a daily or next-day deposit into your account after subtracting its fees.

The bank’s main influence is on settlement timing. Some banks post same-day deposits if batches close before cutoff; others delay a full business day.

Chargebacks, refunds, and reserve holds also flow through here. The merchant provider notifies your bank, and funds can be temporarily withheld.

The Flow

Customer pays through your POS.

POS transmits encrypted data to your merchant provider.

The processor communicates with Visa/Mastercard, which talk to the cardholder’s bank.

Authorization returns in seconds.

End of day: your POS batches all transactions.

Merchant provider deposits net funds into your bank account.

At every step, money moves through someone else’s account before it reaches yours.

How the Relationships Work

Relationship Who Controls It Can You Shop It? Typical Cost Impact POS ↔ Merchant The software vendor Sometimes 0.2–0.5% if locked in Merchant ↔ Bank Merchant provider Always Settlement speed, holds POS ↔ Bank Indirect Limited Reporting convenience

You can usually shop the merchant provider independently. The POS often dictates compatibility, and the bank controls when you see your money.

Integration Options

All-in-One (Square, Toast): Simple setup, higher flat rate, fast payouts.

Modular (Clover, Lightspeed, NCR): Use your own merchant account, better rates, more control.

Enterprise (Authorize.net, Worldpay): Deep integration, negotiable pricing, custom settlements.

When you integrate payments directly with your CRM or accounting platform, reconciliation gets automatic — but always check that your deposit reports match your batch totals to catch fee creep.

Real-World Example

Let’s say you run $60,000/month in card volume.

At 2.9% + 30¢, you’ll pay roughly $1,740/month in fees.

On interchange-plus (2.1% effective), that drops to $1,260/month — a savings of about $6,000/year.

That’s the leverage of understanding how these systems connect.

Key Takeaways

Your POS handles the front end.

Your merchant provider handles authorization and settlement.

Your bank just receives the deposit.

The only part you can truly negotiate is the merchant service markup.

If your effective rate is above 3%, you’re probably paying too much.